|

ý

|

ANNUAL

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

|

|

|

SECURITIES

EXCHANGE ACT OF 1934

|

||

|

For

the fiscal year ended December 31, 2006

|

||

|

OR

|

||

|

o

|

TRANSITION

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

|

|

|

SECURITIES

EXCHANGE ACT OF 1934

|

|

Florida

|

0-13358

|

59-2273542

|

||

|

(State

of Incorporation)

|

(Commission

File Number)

|

(IRS

Employer Identification No.)

|

||

|

217

North Monroe Street, Tallahassee, Florida

|

32301

|

|||

|

(Address

of principal executive offices)

|

(Zip

Code)

|

|||

|

Class

|

Outstanding

at February 28, 2007

|

|

|

Common

Stock, $0.01 par value per share

|

18,388,831

shares

|

|

|

PART

I

|

|

|

|

PAGE

|

|

|

|

|

|

|

|

Item

1.

|

|

|

4

|

|

|

Item

1A.

|

|

|

14

|

|

|

Item

1B.

|

|

|

18

|

|

|

Item

2.

|

|

|

19

|

|

|

Item

3.

|

|

|

19

|

|

|

Item

4.

|

|

|

19

|

|

|

|

|

|

|

|

|

PART

II

|

|

|

|

|

|

Item

5.

|

|

|

19

|

|

|

Item

6.

|

|

|

21

|

|

|

Item

7.

|

|

|

22

|

|

|

Item

7A.

|

|

|

47

|

|

|

Item

8.

|

|

|

49

|

|

|

Item

9.

|

|

|

82

|

|

|

Item

9A.

|

|

|

82

|

|

|

Item

9B.

|

|

|

84

|

|

|

|

|

|

|

|

|

PART

III

|

|

|

|

|

|

|

|

|

|

|

|

Item

10.

|

|

|

84

|

|

|

Item

11.

|

|

|

84

|

|

|

Item

12.

|

|

|

84

|

|

|

Item

13.

|

|

|

85

|

|

|

Item

14.

|

|

|

85

|

|

|

|

|

|

|

|

|

PART

IV

|

|

|

|

|

|

|

|

|

|

|

|

Item

15.

|

|

|

86

|

|

|

|

88

|

|||

| § |

our

ability to integrate the business and operations of companies and

banks

that we have acquired, and those we may acquire in the

future;

|

| § |

our

need and our ability to incur additional debt or equity

financing;

|

| § |

the

strength of the United States economy in general and the strength

of the

local economies in which we conduct operations;

|

| § |

the

accuracy of our financial statement estimates and assumptions;

|

| § |

the

effects of harsh weather conditions, including

hurricanes;

|

| § |

inflation,

interest rate, market and monetary fluctuations;

|

| § |

the

effects of our lack of a diversified loan portfolio, including the

risks

of geographic and industry

concentrations;

|

| § |

the

frequency and magnitude of foreclosure of our

loans;

|

| § |

effect

of changes in the stock market and other capital markets;

|

| § |

legislative

or regulatory changes;

|

| § |

our

ability to comply with the extensive laws and regulations to which

we are

subject;

|

| § |

the

willingness of clients to accept third-party products and services

rather

than our products and services and vice

versa;

|

| § |

changes

in the securities and real estate markets;

|

| § |

increased

competition and its effect on

pricing;

|

| § |

technological

changes;

|

| § |

changes

in monetary and fiscal policies of the U.S.

Government;

|

| § |

the

effects of security breaches and computer viruses that may affect

our

computer systems;

|

| § |

changes

in consumer spending and saving habits;

|

| § |

growth

and profitability of our noninterest income;

|

| § |

changes

in accounting principles, policies, practices or

guidelines;

|

| § |

the

limited trading activity of our common

stock;

|

| § |

the

concentration of ownership of our common

stock;

|

| § |

anti-takeover

provisions under federal and state law as well as our Articles of

Incorporation and our bylaws;

|

| § |

other

risks described from time to time in our filings with the Securities

and

Exchange Commission; and

|

| § |

our

ability to manage the risks involved in the foregoing.

|

| § |

Business

Banking -

The Bank provides banking services to corporations and other business

clients. Credit products are available for a wide variety of general

business purposes, including financing for commercial business properties,

equipment, inventories and accounts receivable, as well as commercial

leasing and letters of credit. Treasury management services and merchant

credit card transaction processing services are also

offered.

|

| § |

Commercial

Real Estate Lending -

The Bank provides a wide range of products to meet the financing

needs of

commercial developers and investors, residential builders and developers,

and community development.

|

| § |

Residential

Real Estate Lending -

The Bank provides products to help meet the home financing needs

of

consumers, including conventional permanent and construction/permanent

(fixed or adjustable rate) financing arrangements, and FHA/VA loan

products. The bank offers both fixed-rate and adjustable rate mortgages

(“ARM”) loans. As of December 31, 2006, approximately 33% of the Bank’s

loan portfolio consisted of ARM

loans.

|

| § |

Retail

Credit -

The Bank provides a full range of loan products to meet the needs

of

consumers, including personal loans, automobile loans, boat/RV loans,

home

equity loans, and credit card

programs.

|

| § |

Institutional

Banking -

The Bank provides banking services to meet the needs of state and

local

governments, public schools and colleges, charities, membership and

not-for-profit associations including customized checking and savings

accounts, cash management systems, tax-exempt loans, lines of credit,

and

term loans.

|

| § |

Retail

Banking - The

Bank provides a full range of consumer banking services, including

checking accounts, savings programs, automated teller machines (“ATMs”),

debit/credit cards, night deposit services, safe deposit facilities,

and

PC/Internet banking. Clients can use the “Star-Line” system to gain

24-hour access to their deposit and loan account information, and

transfer

funds between linked accounts. The Bank is a member of the “Star” ATM

Network that permits banking clients to access cash at ATMs or point

of

sale merchants.

|

|

|

|

Market

Share as of June 30,(1)

|

|

|||||||

|

|

|

2006

|

|

2005

|

|

2004

|

|

|||

|

Florida

|

|

|

|

|

|

|

|

|||

|

Alachua

County(2)

|

|

|

5.6

|

%

|

|

6.3

|

%

|

|

--

|

|

|

Bradford

County

|

|

|

44.6

|

%

|

|

42.6

|

%

|

|

37.1

|

%

|

|

Citrus

County

|

|

|

3.3

|

%

|

|

3.5

|

%

|

|

3.6

|

%

|

|

Clay

County

|

|

|

2.0

|

%

|

|

2.2

|

%

|

|

2.4

|

%

|

|

Dixie

County

|

|

|

20.8

|

%

|

|

17.3

|

%

|

|

16.9

|

%

|

|

Gadsden

County

|

|

|

64.9

|

%

|

|

68.0

|

%

|

|

77.7

|

%

|

|

Gilchrist

County

|

|

|

47.1

|

%

|

|

49.5

|

%

|

|

49.4

|

%

|

|

Gulf

County

|

|

|

14.3

|

%

|

|

19.8

|

%

|

|

22.1

|

%

|

|

Hernando

County

|

|

|

1.5

|

%

|

|

1.4

|

%

|

|

1.3

|

%

|

|

Jefferson

County

|

|

|

24.6

|

%

|

|

24.4

|

%

|

|

24.0

|

%

|

|

Leon

County

|

|

|

18.0

|

%

|

|

17.5

|

%

|

|

17.2

|

%

|

|

Levy

County

|

|

|

34.4

|

%

|

|

33.8

|

%

|

|

34.1

|

%

|

|

Madison

County

|

|

|

14.9

|

%

|

|

15.1

|

%

|

|

17.8

|

%

|

|

Pasco

County

|

|

|

0.2

|

%

|

|

0.3

|

%

|

|

0.4

|

%

|

|

St.

Johns County(2)

|

|

|

1.5

|

%

|

|

2.0

|

|

|

--

|

|

|

Putnam

County

|

|

|

12.3

|

%

|

|

12.3

|

%

|

|

12.5

|

%

|

|

Suwannee

County

|

|

|

11.8

|

%

|

|

7.5

|

%

|

|

7.7

|

%

|

|

Taylor

County

|

|

|

28.6

|

%

|

|

27.9

|

%

|

|

27.4

|

%

|

|

Wakulla

County(3)

|

2.9

|

%

|

--

|

--

|

||||||

|

Washington

County

|

|

|

17.4

|

%

|

|

20.3

|

%

|

|

20.0

|

%

|

|

Georgia(4)

|

|

|

|

|

|

|

|

|

|

|

|

Bibb

County

|

|

|

2.9

|

%

|

|

2.8

|

%

|

|

2.8

|

%

|

|

Burke

County

|

|

|

9.2

|

%

|

|

9.3

|

%

|

|

10.3

|

%

|

|

Grady

County

|

|

|

20.0

|

%

|

|

19.7

|

%

|

|

23.6

|

%

|

|

Laurens

County(5)

|

|

|

23.8

|

%

|

|

33.1

|

%

|

|

41.8

|

%

|

|

Troup

County

|

|

|

8.2

|

%

|

|

7.5

|

%

|

|

8.2

|

%

|

|

Alabama

|

|

|

|

|

|

|

|

|

|

|

|

Chambers

County

|

|

|

4.7

|

%

|

|

3.9

|

%

|

|

4.4

|

%

|

|

(1)

|

Obtained

from the June 30, 2006 FDIC/OTS Summary of Deposits

Report.

|

|

(2)

|

CCB

entered market in May 2005.

|

|

(3)

|

CCB

entered market in December

2005.

|

|

(4)

|

Does

not include Thomas County where Capital City Bank maintains a residential

mortgage lending office only.

|

|

(5)

|

CCB

entered market in October

2004.

|

|

County

|

Number

of

Commercial

Banks

|

Number

of Commercial

Bank

Offices

|

|

Florida

|

|

|

|

Alachua

|

14

|

64

|

|

Bradford

|

3

|

3

|

|

Citrus

|

15

|

46

|

|

Clay

|

11

|

26

|

|

Dixie

|

3

|

4

|

|

Gadsden

|

4

|

6

|

|

Gilchrist

|

3

|

5

|

|

Gulf

|

4

|

6

|

|

Hernando

|

12

|

36

|

|

Jefferson

|

2

|

2

|

|

Leon

|

13

|

78

|

|

Levy

|

3

|

13

|

|

Madison

|

6

|

6

|

|

Pasco

|

18

|

96

|

|

Putnam

|

5

|

11

|

|

St.

Johns

|

19

|

60

|

|

Suwannee

|

4

|

5

|

|

Taylor

|

3

|

4

|

|

Wakulla

|

4

|

9

|

|

Washington

|

4

|

4

|

|

Georgia

|

|

|

|

Bibb

|

10

|

52

|

|

Burke

|

5

|

10

|

|

Grady

|

5

|

8

|

|

Laurens

|

9

|

19

|

|

Troup

|

8

|

17

|

|

Alabama

|

|

|

|

Chambers

|

4

|

8

|

|

Risk

Factors

|

| § |

the

risk characteristics of various classifications of

loans;

|

| § |

previous

loan loss experience;

|

| § |

specific

loans that have loss potential;

|

| § |

delinquency

trends;

|

| § |

estimated

fair market value of the

collateral;

|

| § |

current

economic conditions; and

|

| § |

geographic

and industry loan concentrations.

|

| § |

Commercial

Real Estate Loans.

Repayment is dependent on income being generated in amounts sufficient

to

cover operating expenses and debt service. These loans also involve

greater risk because they are generally not fully amortizing over

a loan

period, but rather have a balloon payment due at maturity. A borrower’s

ability to make a balloon payment typically will depend on being

able to

either refinance the loan or timely sell the underlying property.

|

| § |

Commercial

Loans.

Repayment is generally dependent upon the successful operation of

the

borrower’s business. In addition, the collateral securing the loans may

depreciate over time, be difficult to appraise, illiquid, or fluctuate

in

value based on the success of the

business.

|

| § |

Construction

Loans.

The risk of loss is largely dependent on our initial estimate of

whether

the property’s value at completion equals or exceeds the cost of property

construction and the availability of take-out financing. During the

construction phase, a number of factors can result in delays or cost

overruns. If our estimate is inaccurate or if actual construction

costs

exceed estimates, the value of the property securing our loan may

be

insufficient to ensure full repayment when completed through a permanent

loan or by seizure of collateral.

|

| § |

Consumer

Loans.

Consumer loans (such as personal lines of credit) are collateralized,

if

at all, with assets that may not provide an adequate source of payment

of

the loan due to depreciation, damage, or

loss.

|

| § |

general

or local economic conditions;

|

| § |

neighborhood

values;

|

| § |

interest

rates;

|

| § |

real

estate tax rates;

|

| § |

operating

expenses of the mortgaged

properties;

|

| § |

supply

of and demand for rental units or

properties;

|

| § |

ability

to obtain and maintain adequate occupancy of the

properties;

|

| § |

zoning

laws;

|

| § |

governmental

rules, regulations and fiscal policies;

and

|

| § |

acts

of God.

|

| § |

Supermajority

voting requirements to remove a director from

office;

|

| § |

Provisions

regarding the timing and content of shareowner proposals and

nominations;

|

| § |

Supermajority

voting requirements to amend Articles of Incorporation unless approval

is

received by a majority of “disinterested

directors”;

|

| § |

Absence

of cumulative voting; and

|

| § |

Inability

for shareowners to take action by written

consent.

|

|

Unresolved

Staff Comments

|

|

Properties

|

|

Legal

Proceedings

|

|

Submission

of Matters to a Vote of Security

Holders

|

|

Market

for the Registrant's Common Equity, Related Shareowner Matters, and

Issuer

Purchases of Equity

Securities

|

|

|

|

2006

|

|

2005

|

|

||||||||||||||||||||

|

|

|

Fourth

Qtr.

|

|

Third

Qtr.

|

|

Second

Qtr.

|

|

First

Qtr.

|

|

Fourth

Qtr.

|

|

Third

Qtr.

|

|

Second

Qtr.

|

|

First

Qtr.

|

|

||||||||

|

Common

stock price:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

High

|

|

$

|

35.98

|

|

$

|

33.25

|

|

$

|

35.39

|

|

$

|

37.97

|

|

$

|

39.33

|

|

$

|

38.72

|

|

$

|

33.46

|

|

$

|

33.60

|

|

|

Low

|

|

|

30.14

|

|

|

29.87

|

|

29.51

|

|

|

33.79

|

|

|

33.21

|

|

|

31.78

|

|

|

28.02

|

|

|

29.30

|

|

|

|

Close

|

|

|

35.30

|

|

|

31.10

|

|

|

30.20

|

|

|

35.55

|

|

|

34.29

|

|

|

37.71

|

|

|

32.32

|

|

|

32.41

|

|

|

Cash

dividends declared per share

|

|

|

.1750

|

|

|

.1625

|

|

|

.1625

|

|

|

.1625

|

|

|

.1625

|

|

|

.1520

|

|

|

.1520

|

|

|

.1520

|

|

|

Period

|

Total

number

of

shares

purchased

|

|

Average

price

paid

per

share

|

|

Total

number of

shares

purchased as

part

of our share

repurchase

program(1)

|

|

Maximum

Number

of

shares that

may

yet be purchased

under

our share

repurchase

program

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

October

1, 2006 to October 31, 2006

|

|

-

|

|

|

-

|

|

|

|

-

|

|

|

307,758

|

|

||||||

|

November

1, 2006 to November 30, 2006

|

|

11,581

|

|

|

|

$32.98

|

|

|

|

879,837

|

|

|

|

296,177

|

|

||||

|

December

1, 2006 to December 31, 2006

|

|

4,139

|

|

|

|

32.90

|

|

|

|

883,976

|

|

|

|

292,038

|

|

||||

|

Total

|

|

15,720

|

|

|

|

$32.96

|

|

|

|

883,976

|

|

|

|

292,038

|

|

||||

|

(1)

|

This

balance represents the number of shares that were repurchased through

the

Capital City Bank Group, Inc. Share Repurchase Program, which was

approved

on March 30, 2000, and modified by our Board on January 24, 2002

(the

"Program") under which we were authorized to repurchase up to 1,171,875

shares of our common stock. The Program is flexible and shares are

acquired from the public markets and other sources with either free

cash

flow or borrowed funds. There is no predetermined expiration date

for the

Program.

|

|

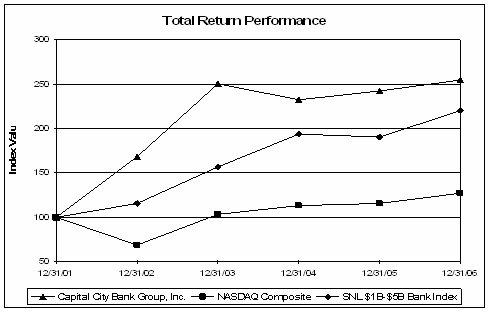

|

Period

Ending

|

|||||

|

Index

|

12/31/01

|

12/31/02

|

12/31/03

|

12/31/04

|

12/31/05

|

12/31/06

|

|

Capital

City Bank Group, Inc.

|

100.00

|

168.06

|

251.02

|

232.18

|

242.31

|

254.43

|

|

NASDAQ

Composite

|

100.00

|

68.76

|

103.67

|

113.16

|

115.57

|

127.58

|

|

SNL

$1B-$5B Bank Index

|

100.00

|

115.44

|

156.98

|

193.74

|

190.43

|

220.36

|

|

|

|

For

the Years Ended December 31,

|

|

|||||||||||||

|

(Dollars

in Thousands, Except Per Share Data)(1)

|

|

2006

|

|

2005

|

|

2004

|

|

2003

|

|

2002

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Interest

Income

|

|

$

|

165,893

|

|

$

|

140,053

|

|

$

|

101,525

|

|

$

|

94,830

|

|

$

|

104,165

|

|

|

Net

Interest Income

|

|

|

119,136

|

|

|

109,990

|

|

|

86,084

|

|

|

79,991

|

|

|

81,662

|

|

|

Provision

for Loan Losses

|

|

|

1,959

|

|

|

2,507

|

|

|

2,141

|

|

|

3,436

|

|

|

3,297

|

|

|

Net

Income

|

|

|

33,265

|

|

|

30,281

|

|

|

29,371

|

|

|

25,193

|

|

|

23,082

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Per

Common Share:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic

Net Income

|

|

$

|

1.79

|

|

$

|

1.66

|

|

$

|

1.74

|

|

$

|

1.53

|

|

$

|

1.40

|

|

|

Diluted

Net Income

|

|

|

1.79

|

|

|

1.66

|

|

|

1.74

|

|

|

1.52

|

|

|

1.39

|

|

|

Cash

Dividends Declared

|

|

|

.663

|

|

|

.619

|

|

|

.584

|

|

|

.525

|

|

|

.402

|

|

|

Book

Value

|

|

|

17.01

|

|

|

16.39

|

|

|

14.51

|

|

|

15.27

|

|

|

14.08

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Key

Performance Ratios:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Return

on Average Assets

|

|

|

1.29

|

%

|

|

1.22

|

%

|

|

1.46

|

%

|

|

1.40

|

%

|

|

1.34

|

%

|

|

Return

on Average Equity

|

|

|

10.48

|

|

|

10.56

|

|

|

13.31

|

|

|

12.82

|

|

|

12.85

|

|

|

Net

Interest Margin (FTE)

|

|

|

5.35

|

|

|

5.09

|

|

|

4.88

|

|

|

5.01

|

|

|

5.35

|

|

|

Dividend

Pay-Out Ratio

|

|

|

37.01

|

|

|

37.35

|

|

|

33.62

|

|

|

34.51

|

|

|

28.87

|

|

|

Equity

to Assets Ratio

|

|

|

12.15

|

|

|

11.65

|

|

|

10.86

|

|

|

10.98

|

|

|

10.22

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Asset

Quality:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Allowance

for Loan Losses

|

|

$

|

17,217

|

|

$

|

17,410

|

|

$

|

16,037

|

|

$

|

12,429

|

|

$

|

12,495

|

|

|

Allowance

for Loan Losses to Loans

|

|

|

0.86

|

%

|

|

0.84

|

%

|

|

0.88

|

%

|

|

0.93

|

%

|

|

0.97

|

%

|

|

Nonperforming

Assets

|

|

|

8,731

|

|

|

5,550

|

|

|

5,271

|

|

|

7,301

|

|

|

3,843

|

|

|

Nonperforming

Assets to Loans + ORE

|

|

|

0.44

|

|

|

0.27

|

|

|

0.29

|

|

|

0.54

|

|

|

0.30

|

|

|

Allowance

to Nonperforming Loans

|

|

|

214.09

|

|

|

331.11

|

|

|

345.18

|

|

|

529.80

|

|

|

497.72

|

|

|

Net

Charge-Offs to Average Loans

|

|

|

0.11

|

|

|

0.13

|

|

|

0.22

|

|

|

0.27

|

|

|

0.23

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Averages

for the Year:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Loans,

Net

|

|

$

|

2,029,397

|

|

$

|

1,968,289

|

|

$

|

1,538,744

|

|

$

|

1,318,080

|

|

$

|

1,256,107

|

|

|

Earning

Assets

|

|

|

2,258,277

|

|

|

2,187,672

|

|

|

1,789,843

|

|

|

1,624,680

|

|

|

1,556,500

|

|

|

Total

Assets

|

|

|

2,581,078

|

|

|

2,486,733

|

|

|

2,006,745

|

|

|

1,804,895

|

|

|

1,727,180

|

|

|

Deposits

|

|

|

2,034,931

|

|

|

1,954,888

|

|

|

1,599,201

|

|

|

1,431,808

|

|

|

1,424,999

|

|

|

Subordinated

Notes

|

|

|

62,887

|

|

|

50,717

|

|

|

5,155

|

|

|

-

|

|

|

-

|

|

|

Long-Term

Borrowings

|

|

|

57,260

|

|

|

70,216

|

|

|

59,462

|

|

|

55,594

|

|

|

30,423

|

|

|

Shareowners'

Equity

|

|

|

317,336

|

|

|

286,712

|

|

|

220,731

|

|

|

196,588

|

|

|

179,652

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Year-End

Balances:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Loans,

Net

|

|

$

|

1,999,721

|

|

$

|

2,067,494

|

|

$

|

1,828,825

|

|

$

|

1,341,632

|

|

$

|

1,285,221

|

|

|

Earning

Assets

|

|

|

2,270,410

|

|

|

2,299,677

|

|

|

2,113,571

|

|

|

1,648,818

|

|

|

1,636,472

|

|

|

Total

Assets

|

|

|

2,597,910

|

|

|

2,625,462

|

|

|

2,364,013

|

|

|

1,846,502

|

|

|

1,824,771

|

|

|

Deposits

|

|

|

2,081,654

|

|

|

2,079,346

|

|

|

1,894,886

|

|

|

1,474,205

|

|

|

1,434,200

|

|

|

Subordinated

Notes

|

|

|

62,887

|

|

|

62,887

|

|

|

30,928

|

|

|

-

|

|

|

-

|

|

|

Long-Term

Borrowings

|

|

|

43,083

|

|

|

69,630

|

|

|

68,453

|

|

|

46,475

|

|

|

71,745

|

|

|

Shareowners'

Equity

|

|

|

315,770

|

|

|

305,776

|

|

|

256,800

|

|

|

202,809

|

|

|

186,531

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Other

Data:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic

Average Shares Outstanding

|

|

|

18,584,519

|

|

|

18,263,855

|

|

|

16,805,696

|

|

|

16,528,109

|

|

|

16,531,606

|

|

|

Diluted

Average Shares Outstanding

|

|

|

18,609,839

|

|

|

18,281,243

|

|

|

16,810,926

|

|

|

16,563,986

|

|

|

16,592,944

|

|

|

Shareowners

of Record(2)

|

|

|

1,805

|

|

|

1,716

|

|

|

1,598

|

|

|

1,512

|

|

|

1,457

|

|

|

Banking

Locations(2)

|

|

|

69

|

|

|

69

|

|

|

60

|

|

|

57

|

|

|

54

|

|

|

Full-Time

Equivalent Associates(2)

|

|

|

1,056

|

|

|

1,013

|

|

|

926

|

|

|

795

|

|

|

781

|

|

|

(1)

|

All

share and per share data have been adjusted to reflect the 5-for-4

stock

split effective July 1, 2005, and the 5-for-4 stock split effective

June

13, 2003.

|

|

(2)

|

As

of the record date. The record date is on or about March 1st of the

following year.

|

|

Management's

Discussion and Analysis of Financial Condition and Results of

Operations

|

|

For

the Years Ended December 31,

|

|||

|

2006

|

2005

|

2004

|

|

|

Efficiency

ratio

|

68.87%

|

68.46%

|

64.73%

|

|

Effect

of intangible amortization and one-time merger expenses

|

(3.45)%

|

(3.67)%

|

(3.17%)

|

|

Operating

efficiency ratio

|

65.42%

|

64.79%

|

61.56%

|

|

For

the Years Ended December 31,

|

|||

|

2006

|

2005

|

2004

|

|

|

Net

noninterest expense as a percent of average assets

|

2.56%

|

2.44%

|

1.93%

|

|

Effect

of intangible amortization and one-time merger expenses

|

(0.24)%

|

(0.24)%

|

(0.22)%

|

|

Operating

net noninterest expense ratio

|

2.32%

|

2.20%

|

1.71%

|

| § |

2006

earnings of $33.3 million, or $1.79 per diluted share, an increase

of 9.9%

and 7.8%, respectively, over 2005.

|

| § |

Growth

in earnings was attributable to strong growth in operating revenues

led by

an 8.3% improvement in net interest income and a 13.0% increase in

noninterest income.

|

| § |

Tax

equivalent net interest income grew 8.8% over 2005 due to growth

in

average earnings assets attributable to the FABC acquisition and

an

improved net interest margin.

|

| § |

Net

interest margin percentage improved 26 basis points over 2005 driven

by

higher earning asset yields and a slight improvement in the earning

asset

mix.

|

| § |

Noninterest

income grew 13.0% over 2005 due primarily to higher deposit fees,

retail

brokerage fees, and card processing

fees.

|

| § |

Strong

credit quality continues to be a key driver in the Bank’s earnings

performance. Net charge-offs totaled $2.1 million, or .11% of average

loans for 2006 compared to $2.5 million, or .13% in 2005. At year-end

the

allowance for loan losses was .86% of outstanding loans and provided

coverage of 214% of nonperforming

loans.

|

| § |

We

remain well-capitalized with a risk based capital ratio of

14.95%.

|

|

|

|

For

the Years Ended December 31,

|

|

|||||||

|

(Dollars

in Thousands, Except Per Share Data)(1)

|

|

2006

|

|

2005

|

|

2004

|

|

|||

|

Interest

Income

|

|

$

|

165,893

|

|

$

|

140,053

|

|

$

|

101,525

|

|

|

Taxable

Equivalent Adjustments

|

|

|

1,812

|

|

|

1,222

|

|

|

1,207

|

|

|

Total

Interest Income (FTE)

|

|

|

167,705

|

|

|

141,275

|

|

|

102,732

|

|

|

Interest

Expense

|

|

|

46,757

|

|

|

30,063

|

|

|

15,441

|

|

|

Net

Interest Income (FTE)

|

|

|

120,948

|

|

|

111,212

|

|

|

87,291

|

|

|

Provision

for Loan Losses

|

|

|

1,959

|

|

|

2,507

|

|

|

2,141

|

|

|

Taxable

Equivalent Adjustments

|

|

|

1,812

|

|

|

1,222

|

|

|

1,207

|

|

|

Net

Interest Income After Provision for Loan Losses

|

|

|

117,177

|

|

|

107,483

|

|

|

83,943

|

|

|

Noninterest

Income

|

|

|

55,577

|

|

|

49,198

|

|

|

43,372

|

|

|

Gain

on Sale of Credit Card Portfolios

|

|

|

-

|

|

|

-

|

|

|

7,181

|

|

|

Noninterest

Expense

|

|

|

121,568

|

|

|

109,814

|

|

|

89,226

|

|

|

Income

Before Income Taxes

|

|

|

51,186

|

|

|

46,867

|

|

|

45,270

|

|

|

Income

Taxes

|

|

|

17,921

|

|

|

16,586

|

|

|

15,899

|

|

|

Net

Income

|

$

|

33,265

|

$

|

30,281

|

$

|

29,371

|

||||

|

Basic

Net Income Per Share

|

$

|

1.79

|

$

|

1.66

|

$

|

1.74

|

||||

|

Diluted

Net Income Per Share

|

$

|

1.79

|

$

|

1.66

|

$

|

1.74

|

||||

|

(1)

|

All

share and per share data have been adjusted to reflect the 5-for-4

stock

split effective July 1, 2005.

|

|

|

|

2006

|

|

2005

|

|

2004

|

|

|||||||||||||||||||||

|

(Taxable

Equivalent Basis - Dollars in Thousands)

|

|

Balance

|

|

Interest

|

|

Rate

|

|

Balance

|

|

Interest

|

|

Rate

|

|

Balance

|

|

Interest

|

|

Rate

|

|

|||||||||

|

ASSETS

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

Loans,

Net of Unearned Interest(1)(2)

|

|

$

|

2,029,397

|

|

$

|

157,227

|

|

|

7.75

|

%

|

$

|

1,968,289

|

|

$

|

133,665

|

|

|

6.79

|

%

|

$

|

1,538,744

|

|

$

|

95,796

|

|

|

6.23

|

%

|

|

Taxable

Investment Securities

|

|

|

112,392

|

|

|

4,851

|

|

|

4.31

|

%

|

|

142,406

|

|

|

4,250

|

|

|

2.98

|

%

|

|

131,842

|

|

|

3,138

|

|

|

2.38

|

%

|

|

Tax-Exempt

Investment Securities(2)

|

|

|

74,634

|

|

|

3,588

|

|

|

4.81

|

%

|

|

49,252

|

|

|

2,369

|

|

|

4.81

|

%

|

|

51,979

|

|

|

2,965

|

|

|

5.70

|

%

|

|

Funds

Sold

|

|

|

41,854

|

|

|

2,039

|

|

|

4.81

|

%

|

|

27,725

|

|

|

991

|

|

|

3.53

|

%

|

|

67,278

|

|

|

833

|

|

|

1.24

|

%

|

|

Total

Earning Assets

|

|

|

2,258,277

|

|

|

167,705

|

|

|

7.42

|

%

|

|

2,187,672

|

|

|

141,275

|

|

|

6.46

|

%

|

|

1,789,843

|

|

|

102,732

|

|

|

5.74

|

%

|

|

Cash

& Due From Banks

|

|

|

100,237

|

|

|

|

|

|

|

|

|

105,787

|

|

|

|

|

|

|

|

|

93,070

|

|

|

|

|

|

|

|

|

Allowance

for Loan Losses

|

|

|

(17,486

|

)

|

|

|

|

|

|

|

|

(17,081

|

)

|

|

|

|

|

|

|

|

(13,846

|

)

|

|

|

|

|

|

|

|

Other

Assets

|

|

|

240,050

|

|

|

|

|

|

|

|

|

210,355

|

|

|

|

|

|

|

|

|

137,678

|

|

|

|

|

|

|

|

|

TOTAL

ASSETS

|

|

$

|

2,581,078

|

|

|

|

|

|

|

|

$

|

2,486,733

|

|

|

|

|

|

|

|

$

|

2,006,745

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

LIABILITIES

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NOW

Accounts

|

|

$

|

518,671

|

|

$

|

7,658

|

|

|

1.48

|

%

|

$

|

430,601

|

|

$

|

2,868

|

|

|

.67

|

%

|

$

|

292,492

|

|

$

|

733

|

|

|

.25

|

%

|

|

Money

Market Accounts

|

|

|

370,257

|

|

|

11,687

|

|

|

3.16

|

%

|

|

275,830

|

|

|

4,337

|

|

|

1.57

|

%

|

|

227,808

|

|

|

1,190

|

|

|

.52

|

%

|

|

Savings

Accounts

|

|

|

134,033

|

|

|

278

|

|

|

0.21

|

%

|

|

152,890

|

|

|

292

|

|

|

0.19

|

%

|

|

130,282

|

|

|

164

|

|

|

.13

|

%

|

|

Other

Time Deposits

|

|

|

507,283

|

|

|

17,630

|

|

|

3.48

|

%

|

|

550,821

|

|

|

13,637

|

|

|

2.48

|

%

|

|

459,464

|

|

|

9,228

|

|

|

2.01

|

%

|

|

Total

Int. Bearing Deposits

|

|

|

1,530,244

|

|

|

37,253

|

|

|

2.43

|

%

|

|

1,410,142

|

|

|

21,134

|

|

|

1.50

|

%

|

|

1,110,046

|

|

|

11,315

|

|

|

1.02

|

%

|

|

Short-Term

Borrowings

|

|

|

78,700

|

|

|

3,074

|

|

|

3.89

|

%

|

|

97,863

|

|

|

2,854

|

|

|

2.92

|

%

|

|

100,582

|

|

|

1,270

|

|

|

1.26

|

%

|

|

Subordinated

Notes Payable

|

|

|

62,887

|

|

|

3,725

|

|

|

5.92

|

%

|

|

50,717

|

|

|

2,981

|

|

|

5.88

|

%

|

|

5,155

|

|

|

294

|

|

|

5.71

|

%

|

|

Other

Long-Term Borrowings

|

|

|

57,260

|

|

|

2,705

|

|

|

4.72

|

%

|

|

70,216

|

|

|

3,094

|

|

|

4.41

|

%

|

|

59,462

|

|

|

2,562

|

|

|

4.31

|

%

|

|

Total

Int. Bearing Liabilities

|

|

|

1,729,091

|

|

|

46,757

|

|

|

2.70

|

%

|

|

1,628,938

|

|

|

30,063

|

|

|

1.85

|

%

|

|

1,275,245

|

|

|

15,441

|

|

|

1.21

|

%

|

|

Noninterest

Bearing Deposits

|

|

|

504,687

|

|

|

|

|

|

|

|

|

544,746

|

|

|

|

|

|

|

|

|

489,155

|

|

|

|

|

|

|

|

|

Other

Liabilities

|

|

|

29,964

|

|

|

|

|

|

|

|

|

26,337

|

|

|

|

|

|

|

|

|

21,614

|

|

|

|

|

|

|

|

|

TOTAL

LIABILITIES

|

|

|

2,263,742

|

|

|

|

|

|

|

|

|

2,200,021

|

|

|

|

|

|

|

|

|

1,786,014

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SHAREOWNERS'

EQUITY

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TOTAL

SHAREOWNERS' EQUITY

|

|

|

317,336

|

|

|

|

|

|

|

|

|

286,712

|

|

|

|

|

|

|

|

|

220,731

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TOTAL

LIABILITIES & EQUITY

|

|

$

|

2,581,078

|

|

|

|

|

|

|

|

$

|

2,486,733

|

|

|

|

|

|

|

|

$

|

2,006,745

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest

Rate Spread

|

|

|

|

|

|

|

|

|

4.72

|

%

|

|

|

|

|

|

|

|

4.61

|

%

|

|

|

|

|

|

|

|

4.53

|

%

|

|

Net

Interest Income

|

|

|

|

|

$

|

120,948

|

|

|

|

|

|

|

|

$

|

111,212

|

|

|

|

|

|

|

|

$

|

87,291

|

|

|

|

|

|

Net

Interest Margin(3)

|

|

|

|

|

|

|

|

|

5.35

|

%

|

|

|

|

|

|

|

|

5.09

|

%

|

|

|

|

|

|

|

|

4.88

|

%

|

|

(1)

|

Average

balances include nonaccrual loans. Interest income includes loan

fees of

$3.8 million, $3.1 million, and $1.7 million in 2006, 2005, and 2004,

respectively.

|

|

(2)

|

Interest

income includes the effects of taxable equivalent adjustments using

a 35%

tax rate.

|

|

(3)

|

Taxable

equivalent net interest income divided by average earning

assets.

|

|

|

|

2006

Changes From 2005

|

|

2005

Changes From 2004

|

|

||||||||||||||||||||||||||||

|

|

|

|

|

Due

to Average

|

|

|

|

Due

to Average

|

|

||||||||||||||||||||||||

|

(Taxable

Equivalent Basis - Dollars in Thousands)

|

|

Total

|

|

Volume

|

|

Rate

|

|

Total

|

|

Calendar

(3)

|

|

Volume

|

|

Rate

|

|

||||||||||||||||||

|

Earning

Assets:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

Loans,

Net of Unearned Interest (2)

|

|

$

|

23,562

|

|

$

|

5,760

|

|

$

|

17,802

|

|

$

|

37,870

|

|

$

|

(262

|

)

|

$

|

27,706

|

|

$

|

11,506

|

|

|||||||||||

|

Investment

Securities:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

Taxable

|

|

|

601

|

|

|

(689

|

)

|

|

1,290

|

|

|

1,110

|

|

|

(3

|

)

|

|

693

|

|

|

420

|

|

|||||||||||

|

Tax-Exempt

(2)

|

|

|

1,219

|

|

|

1,220

|

|

|

(1

|

)

|

|

(597

|

)

|

|

-

|

|

|

(156

|

)

|

|

(441

|

)

|

|||||||||||

|

Funds

Sold

|

|

|

1,048

|

|

|

444

|

|

|

604

|

|

|

158

|

|

|

(2

|

)

|

|

(488

|

)

|

|

648

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

Total

|

|

|

26,430

|

|

|

6,735

|

|

|

19,695

|

|

|

38,541

|

|

|

(267

|

)

|

|

27,125

|

|

|

11,683

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

Interest

Bearing Liabilities:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

NOW

Accounts

|

|

|

4,790

|

|

|

586

|

|

|

4,204

|

|

|

2,134

|

|

|

(2

|

)

|

|

347

|

|

|

1,789

|

|

|||||||||||

|

Money

Market Accounts

|

|

|

7,350

|

|

|

1,485

|

|

|

5,865

|

|

|

3,148

|

|

|

(3

|

)

|

|

251

|

|

|

2,900

|

|

|||||||||||

|

Savings

Accounts

|

|

|

(14

|

)

|

|

(36

|

)

|

|

22

|

|

|

128

|

|

|

(1

|

)

|

|

28

|

|

|

101

|

|

|||||||||||

|

Time

Deposits

|

|

|

3,993

|

|

|

(1,078

|

)

|

|

5,071

|

|

|

4,408

|

|

|

(25

|

)

|

|

1,840

|

|

|

2,593

|

|

|||||||||||

|

Short-Term

Borrowings

|

|

|

221

|

|

|

(586

|

)

|

|

807

|

|

|

1,585

|

|

|

(3

|

)

|

|

83

|

|

|

1,505

|

|

|||||||||||

|

Subordinated

Notes Payable

|

|

|

744

|

|

|

715

|

|

|

29

|

|

|

2,687

|

|

|

(1

|

)

|

|

2,609

|

|

|

79

|

|

|||||||||||

|

Long-Term

Borrowings

|

|

|

(390

|

)

|

|

(571

|

)

|

|

181

|

|

|

532

|

|

|

(7

|

)

|

|

465

|

|

|

74

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

Total

|

|

|

16,694

|

|

|

515

|

|

|

16,179

|

|

|

14,622

|

|

|

(42

|

)

|

|

5,623

|

|

|

9,041

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

Changes

in Net Interest Income

|

|

$

|

9,736

|

|

$

|

6,220

|

|

$

|

3,516

|

|

$

|

23,919

|

|

$

|

(255

|

)

|

$

|

21,502

|

|

$

|

2,642

|

|

|||||||||||

|

(1)

|

This

table shows the change in taxable equivalent net interest income

for

comparative periods based on either changes in average volume or

changes

in average rates for earning assets and interest bearing liabilities.

Changes which are not solely due to volume changes or solely due

to rate

changes have been attributed to rate changes.

|

|

(2)

|

Interest

income includes the effects of taxable equivalent adjustments using

a 35%

tax rate to adjust interest on tax-exempt loans and securities to

a

taxable equivalent basis.

|

|

|

|

For

the Years Ended December 31,

|

|||||||

|

(Dollars

in Thousands)

|

|

2006

|

|

2005

|

|

2004

|

|||

|

Noninterest

Income:

|

|

|

|

|

|

|

|||

|

Service

Charges on Deposit Accounts

|

|

$

|

24,620

|

|

$

|

20,740

|

|

$

|

17,574

|

|

Data

Processing

|

|

|

2,723

|

|

|

2,610

|

|

|

2,628

|

|

Asset

Management Fees

|

|

|

4,600

|

|

|

4,419

|

|

|

4,007

|

|

Retail

Brokerage Fees

|

|

|

2,091

|

|

|

1,322

|

|

|

1,401

|

|

(Loss)/Gain

on Sale of Investment Securities

|

(4)

|

9

|

14

|

||||||

|

Mortgage

Banking Revenues

|

|

|

3,235

|

|

|

4,072

|

|

|

3,208

|

|

Merchant

Services Fees

|

|

|

6,978

|

|

|

6,174

|

|

|

5,135

|

|

Interchange

Fees

|

|

|

3,105

|

|

|

2,239

|

|

|

2,229

|

|

Gain

on Sale of Credit Card Portfolios

|

-

|

-

|

7,180

|

||||||

|

ATM/Debit

Card Fees

|

|

|

2,519

|

|

|

2,206

|

|

|

2,007

|

|

Other

|

|

|

5,710

|

|

|

5,407

|

|

|

5,170

|

|

Total

Noninterest Income

|

|

$

|

55,577

|

|

$

|

49,198

|

|

$

|

50,553

|

|

|

|

For

the Years Ended December 31,

|

|||||||

|

(Dollars

in Thousands)

|

|

2006

|

|

2005

|

|

2004

|

|||

|

Noninterest

Expense:

|

|

|

|

|

|

|

|||

|

Salaries

|

|

$

|

46,604

|

|

$

|

40,978

|

|

$

|

33,968

|

|

Associate

Benefits

|

|

|

14,251

|

|

|

12,709

|

|

|

10,377

|

|

Total

Compensation

|

|

|

60,855

|

|

|

53,687

|

|

|

44,345

|

|

|

|

|

|

|

|

|

|

|

|

|

Premises

|

|

|

9,395

|

|

|

8,293

|

|

|

7,074

|

|

Equipment

|

|

|

9,911

|

|

|

8,970

|

|

|

8,393

|

|

Total

Occupancy

|

|

|

19,306

|

|

|

17,263

|

|

|

15,467

|

|

|

|

|

|

|

|

|

|

|

|

|

Legal

Fees

|

|

|

1,734

|

|

|

1,827

|

|

|

1,301

|

|

Professional

Fees

|

|

|

3,402

|

|

|

3,825

|

|

|

2,858

|

|

Processing

Services

|

|

|

1,863

|

|

|

1,481

|

|

|

997

|

|

Advertising

|

|

|

4,285

|

|

|

4,275

|

|

|

2,001

|

|

Travel

and Entertainment

|

|

|

1,664

|

|

|

1,414

|

|

|

1,023

|

|

Printing

and Supplies

|

|

|

2,472

|

|

|

2,372

|

|

|

1,854

|

|

Telephone

|

|

|

2,323

|

|

|

2,493

|

|

|

2,048

|

|

Postage

|

|

|

1,145

|

|

|

1,195

|

|

|

1,007

|

|

Intangible

Amortization

|

|

|

6,085

|

|

|

5,440

|

|

|

3,824

|

|

Merger

Expense

|

-

|

438

|

550

|

||||||

|

Interchange

Fees

|

|

|

6,010

|

|

|

5,402

|

|

|

4,741

|

|

Courier

Service

|

|

|

1,307

|

|

|

1,360

|

|

|

1,143

|

|

Miscellaneous

|

|

|

9,117

|

|

|

7,342

|

|

|

6,067

|

|

Total

Other

|

41,407

|

38,864

|

29,414

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

Total

Noninterest Expense

|

|

$

|

121,568

|

|

$

|

109,814

|

|

$

|

89,226

|

|

2005

to

|

Percentage

|

Components

of

|

||||||

|

2006

|

Of

Total

|

Average

|

Earning

|

Assets

|

||||

|

(Average

Balances - Dollars In Thousands)

|

Change

|

Change

|

2006

|

2005

|

2004

|

|||

|

Loans:

|

||||||||

|

Commercial,

Financial, and Agricultural

|

$

11,642

|

16.0%

|

9.7%

|

9.5%

|

10.3%

|

|||

|

Real

Estate - Construction

|

23,811

|

34.0%

|

7.8%

|

6.9%

|

6.2%

|

|||

|

Real

Estate - Commercial

|

(20,392)

|

(29.0%)

|

29.5%

|

31.4%

|

27.3%

|

|||

|

Real

Estate - Residential

|

42,022

|

60.0%

|

32.2%

|

31.3%

|

29.1%

|

|||

|

Consumer

|

4,025

|

6.0%

|

10.7%

|

10.9%

|

13.1%

|

|||

|

Total

Loans

|

61,108

|

87.0%

|

89.9%

|

90.0%

|

86.0%

|

|||

|

Investment

Securities:

|

||||||||

|

Taxable

|

(30,014)

|

(43.0%)

|

5.0%

|

6.5%

|

7.4%

|

|||

|

Tax-Exempt

|

25,382

|

36.0%

|

3.2%

|

2.3%

|

2.9%

|

|||

|

Total

Securities

|

(4,632)

|

(7.0%)

|

8.2%

|

8.8%

|

10.3%

|

|||

|

Funds

Sold

|

14,129

|

20.0%

|

1.9%

|

1.2%

|

3.7%

|

|||

|

Total

Earning Assets

|

$

70,605

|

100.0%

|

100.0%

|

100.0%

|

100.0%

|

|||

|

|

|

As

of December 31,

|

|

|||||||||||||

|

(Dollars

in Thousands)

|

|

2006

|

2005

|

2004

|

2003

|

2002

|

|

|||||||||

|

Commercial,

Financial and Agricultural

|

|

$

|

229,327

|

$

|

218,434

|

$

|

206,474

|

$

|

160,048

|

$

|

141,459

|

|

||||

|

Real

Estate - Construction

|

|

|

179,072

|

160,914

|

140,190

|

89,149

|

91,110

|

|

||||||||

|

Real

Estate - Commercial

|

|

|

643,885

|

718,741

|

655,426

|

391,250

|

356,807

|

|

||||||||

|

Real

Estate - Residential

|

|

|

709,735

|

723,336

|

600,375

|

467,790

|

474,069

|

|

||||||||

|

Consumer

|

|

|

237,702

|

246,069

|

226,360

|

233,395

|

221,776

|

|

||||||||

|

Total

Loans, Net of Unearned Interest

|

|

$

|

1,999,721

|

$

|

2,067,494

|

$

|

1,828,825

|

$

|

1,341,632

|

$

|

1,285,221

|

|

||||

|

|

|

Maturity

Periods

|

|

||||||||||

|

(Dollars

in Thousands)

|

|

One

Year

or

Less

|

|

Over

One

Through

Five

Years

|

|

Over

Five

Years

|

|

Total

|

|

||||

|

Commercial,

Financial and Agricultural

|

|

$

|

96,103

|

96,313

|

36,911

|

229,327

|

|

||||||

|

Real

Estate

|

|

|

456,980

|

225,088

|

850,624

|

1,532,692

|

|

||||||

|

Consumer(1)

|

|

|

31,788

|

201,772

|

4,142

|

237,702

|

|

||||||

|

Total

|

|